Statement of Carolyn W. Colvin,

Acting Commissioner

Social Security Administration

Before the Senate Budget Committee

February 11, 2015

Chairman Enzi, Ranking Member Sanders, and Members of the Committee:

Thank you for the opportunity to discuss the status of the Social Security Disability Insurance Trust Fund, the steps we have taken to ensure the integrity of Disability Determination Services (DDS) and Administrative Law Judge (ALJ) decisions, our efforts to help people with disabilities reenter or stay in the workforce, and our Continuing Disability Review process. My name is Carolyn Colvin, and I am the Acting Commissioner of Social Security.

Throughout my career, I have met people from all walks of life who struggle to cope with severe disabilities. Whether their impairments are mental or physical, by birth or circumstance, these individuals face extraordinary challenges. We must never underestimate the very real challenges and the day to day struggles faced by people with disabilities.

Introduction

The Social Security Administration (SSA) administers a number of programs, including the Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) programs, commonly referred to as “Social Security.” Social Security is a social insurance program, under which workers earn coverage for retirement, survivors, and disability benefits by working and paying Social Security taxes on their earnings. The DI portion of Social Security helps replace a portion of the lost earnings for workers who, due to their significant health problems, can no longer work to support themselves and their families. DI also ensures that workers who become disabled and their families are protected from the loss of future retirement benefits.

The same people who may be receiving disability today at 55 will be receiving retirement benefits later.

We take our responsibilities in administering Social Security very seriously. In 2014, we paid $698 billion to more than 47 million retirement and survivor beneficiaries, and $141 billion to nearly 11 million DI beneficiaries and their family members. We administer the Social Security program with tremendous efficiency. For example, in Fiscal Year (FY) 2014, our administrative expenses were only around 0.6 percent of the Social Security benefits we paid for the year.

The vitally important DI program, however, will face challenges next year in its ability to provide for those workers who are insured for coverage and have severe physical or mental impairments. The challenges for the Trust Fund have been well understood and projected for decades. In 1995, right after the last tax-rate reallocation enacted by the Congress, the Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds estimated that the DI fund reserves would become depleted in 2016.1 This shortfall, the Trustees predicted, was related to demographic changes that could be seen far in advance, such as the entry of more women into the workforce, and the progression of the baby boom generation into its most disability-prone years.

These projections from 20 years ago have proven to be quite accurate. According to the 2014 Annual Trustees Report, the Trustees again project that the DI Trust Fund reserves will reach depletion in the last quarter of 2016. If Congress takes no action before this time, we would only be able to pay about 81 percent of scheduled amounts, resulting in benefit cuts. Cutting these benefits would create hardships for a segment of our society that is ill-equipped to endure them. Therefore, the Administration is committed to working with Congress to prevent the reserve depletion of the DI Trust Fund next year, while continuing to discuss longer-term solutions that would address broader solvency issues that are still many years away.

DI Trust Fund

As I mentioned earlier, the Social Security DI Program provides insurance coverage to the families of workers who have paid into the system and subsequently have become disabled. The FY 2016 President’s Budget proposes to address the near-term DI reserve depletion by reallocating a portion of payroll taxes from OASI to the DI Trust Fund – as has been done many times in the past – to align the reserve depletion dates for the two trust funds. This temporary reallocation will have no effect on the overall health of the combined OASI and DI trust funds, which will remain adequately financed until 2033 on a combined basis. Note that the 2033 reserve depletion date is the one policymakers and the public most often focus on, because they appropriately focus on the Social Security program as a whole.

We believe that the Congress must take action to reallocate a portion of the payroll tax rate between the trust funds to avoid deep and abrupt cuts or delays in benefits for individuals with disabilities who paid into the system while they worked and now need help. The proposal to reallocate payroll tax collections on a temporary basis between the OASI and DI trust funds is consistent with past congressional action, where Congress has approved legislation as needed for reallocation from DI to OASI, and vice versa.2

The FY 2016 President’s Budget includes a reallocation proposal. In our Budget proposal, the reallocation lasts for five years and the share of the total payroll tax going to the DI trust fund increases by 0.9 percentage points. Under this formulation, the reallocation only needs to last five years for the two trust funds to both be able to provide full benefits until 2033. We look forward to working with Congress on the specifics. Workers and employers would continue to have the same FICA deducted, but a somewhat larger share would go to DI than to OASI on a temporary basis to bring the two trust funds into alignment. We look forward to working with the Congress on proposals that would strengthen Social Security for Americans, including current beneficiaries.

Factors Affecting the DI Trust Fund

The proposed reallocation of payroll taxes from OASI to DI need only be temporary because – measured over 75 years – the DI trust fund shortfall is actually slightly smaller as a percentage of dedicated payroll taxes. Moreover, DI and OASI are experiencing the same demographic transition, but because individuals qualify for DI at a younger age than eligibility for retirement benefits, that program experiences the full effects first, since the Baby Boom generation has already reached its peak disability years.

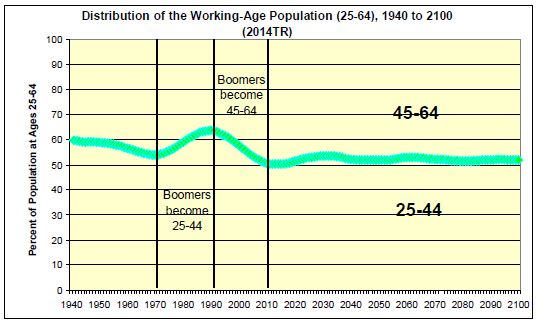

As our Chief Actuary, Stephen C. Goss, accompanying me here today, has explained: the growth in the SSDI rolls has long been foreseen and, as expected, has recently slowed. Between 1980 and 2010, the number of disabled worker beneficiaries increased from 2.9 million to 8.2 million. As I noted earlier, nearly all of the growth in the SSDI rolls over this 30-year period can be attributed to a combination of foreseen factors. The first factor is the 41 percent increase from 1980 to 2010 in the total population between the ages of 20 and 64. A second important factor is the changing age distribution of the population, due to the aging of the baby boomers. Specifically, from 1990 to 2010, the baby boomers moved from being young adults, under age 45, to older working adults, ages 45-64, and the ages at which workers become more disability-prone. This anticipated demographic shift has now finished. (See figure 1)

Figure 1.

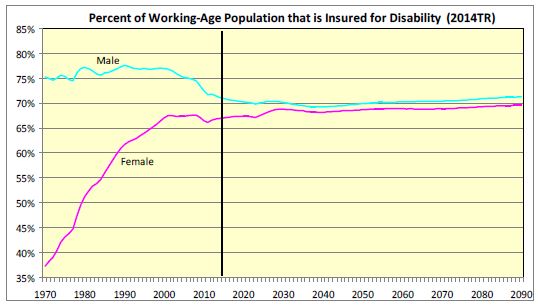

Another important factor is the increased participation of women in the labor force, which has resulted in many more women being insured for disability (see figure 2). The growth of women in the labor force has contributed positively to economic growth and the fact that these workers have protection against disability is a net positive for their families’ economic security.

Figure 2.

Between 1980 and 2010, the percent of the working-age population (approximately 20-65) that was insured rose from about 50 to 68 percent for women.

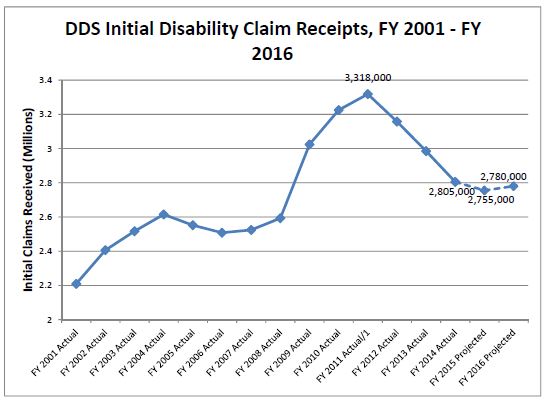

These major factors, in combination with other demographic shifts, are now stabilizing. Indeed, applications for disability benefits have fallen from peak levels of around 3.3 million in FY 2011, to around 2.8 million in FY 2014 (see Figure 3). Mr. Goss is available to explain these foreseen demographic shifts, and the recent slowing of the growth of DI, in greater detail.

Figure 3.

Overview of the DI Program

In addition to discussing the DI Trust Fund, I would like to share with you information concerning the stringent requirements an applicant must meet to qualify for disability benefits, as well as a general overview of the application process.

Definition of Disability

The Social Security Act (Act) generally defines disability as the inability to engage in any substantial gainful activity (SGA) due to a physical or mental impairment that has lasted or is expected to last at least one year or to result in death. Under the Act’s strict standard, a worker can qualify for DI benefits only if he or she is insured for Social Security disability protection – meaning they worked substantially in 5 of the past 10 years before becoming disabled3 – and cannot currently work due to a medically determinable impairment. As the House Committee on Ways and Means noted in its report that accompanied the Social Security Amendments of 1956, even a person with a severe impairment cannot receive disability benefits if he or she can engage in any SGA. The Act does not provide short-term or partial disability benefits.

I would like to stress a salient and often overlooked feature of the DI program. An applicant cannot be found eligible and receive disability benefits simply by alleging pain or other non-exertional limitations. We require objective medical evidence or laboratory findings that show the claimant has a medically determinable impairment(s) that: (1) could reasonably be expected to produce the pain or other symptoms alleged; and (2) when considered with all other evidence, meets our disability requirements.

Because the Act defines disability so strictly, Social Security disability beneficiaries have among the most severe impairments in the country. To give some idea of the standard’s stringency, the allowance rate for disability claims in FY 2013 was around 33 percent.4 While around 30 million Americans ages 21 to 64 self-reported as living with disabilities in the 2010 census,5 in that same year only about 8 million workers received DI payments. Those who receive DI benefits are more than three times as likely to die in a year as other people the same age. Among those who start receiving disability benefits at the age of 55, one in five men and one in seven women die within five years of the onset of their disabilities.

The Claims Process

We take our responsibility to be good stewards of the DI trust funds and taxpayers’ money very seriously and strive to provide the highest quality service possible. When we receive a claim for disability benefits, we strive to make the correct decision as early in the process as possible so that a person who qualifies for DI benefits receives them in a timely manner. We decide claims for benefits using an administrative review process that consists of four levels: (1) initial determination; (2) reconsideration; (3) hearing before an ALJ; and (4) Appeals Council (AC) review. At each level, the decision-maker bases his or her decisions on the medical and other evidence in the record, the Act, and our regulations and policies.

When evaluating disability claims, every decision-maker must use the strict definition of disability set forth in the Act and our regulations and policies. We have multiple layers of quality review to ensure that our program rules are applied uniformly and correctly. In addition, as required by the Act, we perform a pre- effectuation review of at least 50 percent of all initial and reconsideration disability allowances. These pre-effectuation reviews allow us to correct errors we find before we issue a payment. Estimates show the return on investment of roughly $13 in program savings for every $1 of the total cost of the reviews.6

We are continuously developing and improving training and tools to ensure that our adjudicators follow established policies accurately and consistently. For example, at the initial and reconsideration levels, our decision makers use the Electronic Claims Analysis Tool, a web-based application that helps ensure policy compliance by requiring examiners to follow the necessary steps in our disability claims evaluation process. The tool aids in documenting, analyzing, and adjudicating each disability claim according to our regulations.

We now have initiated use of a similar tool – the Electronic Bench Book – at the hearing level. Additionally, for several years we have employed a hearing-level tool that gives adjudicators extensive information about the reasons their favorable and unfavorable decisions were subsequently remanded and allows them to view their performance in relation to the performance of other ALJs in the office, region, and Nation. More recently, we have been incorporating the use of data analytics as another tool to ensure consistent policy compliance and real-time feedback. All of these efforts build on our longstanding commitment and effort to ensure that we provide claimants – who are insured for Social Security coverage – the right decision as quickly as possible.

Return to Work

As I have discussed, the DI program, together with OASI, provides insured coverage for those Americans who make up a very vulnerable segment of society. While the DI program constitutes a part of our Nation’s social insurance, the level of benefits is modest. For example, in January 2015, a worker eligible for DI receives, on average, less than $1,200 in DI benefits per month, or less than $14,000 per year – just above the poverty line. Such DI beneficiary who returns to work may be able to improve upon the modest standard of living provided by DI benefits.

The Social Security Act includes a number of incentives to encourage disability beneficiaries to return to work. Generally, these incentives provide beneficiaries with continued benefits and medical coverage while working or pursuing an employment goal. For example, in the DI program, the incentives include the trial work period, the exclusion of impairment-related work expenses, the extended period of eligibility, and the expedited reinstatement process.7 In the Ticket to Work and Work Incentives Improvement Act of 1999, Congress also created ways for individuals to maintain their Medicare longer or obtain Medicaid coverage even after they have become fully self-supporting and transitioned from the benefit rolls.8 The Ticket Act also gave beneficiaries more choices to obtain employment services and supports. Beneficiaries could, as before, receive services through State Vocational Rehabilitation agencies or seek assistance from newly formed Employment Networks.

We must not downplay or dismiss the very real difficulties beneficiaries with disabilities face. Because the Act defines disability so stringently, DI beneficiaries have significant disabilities. Realistically, we cannot expect that more than a modest share will return to work or leave the benefit rolls due to substantial earnings. But we must continue to assist those beneficiaries who can retain employment or are able to return to work to do so.

Given the number of individuals who ultimately turn to DI for income security and the cost of the program, it is critical for policymakers to have an evidentiary base from which to consider potential program innovations that would improve the ability of individuals with disabilities to succeed in the workforce. We believe conducting demonstration projects is the best way to gather the evidence needed to evaluate policy options.

We have already tested various initiatives that support DI beneficiaries, so a partial evidence base for policy innovation exists. For instance, the Accelerated Benefits demonstration found that providing health benefits to uninsured DI beneficiaries in the 24-month Medicare waiting period sharply improved their self-reported health status, and providing employment services increased work and earnings. The Mental Health Treatment Study (MHTS) demonstration found that employment supports, along with medical support and coordinated care, were successful in improving health, lowering hospitalizations, and increasing employment for DI beneficiaries with schizophrenia and other affective disorders. Other initiatives, such as the Youth Transition Demonstration, have found that support services can increase employment and earnings for younger beneficiaries.

While our demonstrations have shown that interventions for individuals receiving DI benefits can yield positive outcomes, they also show that not all of these interventions help DI beneficiaries return to full-time employment and leave the DI program. For example, relative to the control group, the beneficiaries who received services in the MHTS were more likely to be employed, but their earnings did not typically rise above SGA and reduce their DI benefits. In other words, comprehensive services to individuals already in the program had positive outcomes, but not at a level that would indicate departure from the disability program was likely.

Earlier interventions, before an individual enters the DI rolls may prove more effective. Consequently, the FY 2016 President’s Budget provides continued support for a multi-year initiative for SSA to test innovative strategies to help people with disabilities remain and succeed in the workforce. We appreciate Congress’s $35 million appropriation in FY 2015 to begin this effort, and we look forward to quickly making progress on this initiative. This year’s Budget includes a request for $50 million in FY 2016, and a legislative proposal requesting $350 million total in mandatory funding for FYs 2017-2020 in conjunction with a reauthorization of the larger DI demonstration authority.

Specifically, we propose to partner with other Federal agencies and the public workforce system to test innovative strategies to help people with disabilities remain in the workforce. Early intervention measures, such as supportive employment services for individuals with mental impairments, targeted incentives for employers to help workers with disabilities remain on the job, and incentives and opportunities for States to coordinate services better, have the potential to achieve long-term gains in employment and improve the quality of life of people with disabilities. These proposed demonstrations will help build the evidentiary base for future program improvements.

Program Integrity Initiatives

The FY 2016 President’s Budget contains another important proposal to strengthen the DI program. There is a long-standing adage in our agency – the right check to the right person at the right time. Delivering on this statement preserves the public's trust in our programs. Accordingly, we continually refine a program integrity tools.

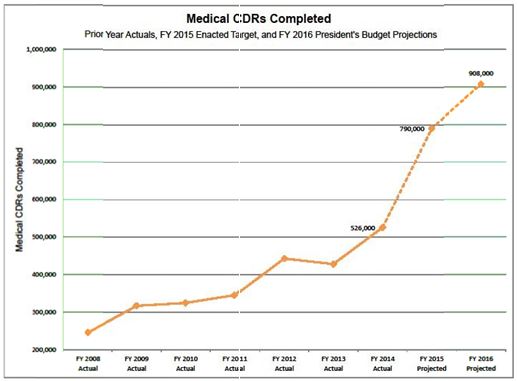

We use Continuing Disability Reviews (CDRs) to determine whether an individual continues to be disabled under the criteria for the DI and Supplemental Security Income Disability programs. We use sophisticated predictive models to ensure that we prioritize reviewing cases where beneficiaries are more likely to have medically improved and are capable of working, which may mean that they are no longer eligible to receive DI or SSI benefits. We estimate that CDRs conducted in FY 2016 will yield a return-on-investment of about $9 on average in net Federal program savings over ten years per $1 budgeted for dedicated program integrity funding, including OASDI, SSI, Medicare, and Medicaid program effects.

In FY 2016, we are using our dedicated program integrity funding for the direct costs of processing CDRs. We will be able to increase the number of full medical CDRs by approximately 15 percent over FY 2015 while continuing to handle a high volume of initial disability claims. We plan to complete 908,000 full medical CDRs in FY 2016 (see Figure 4).

Figure 4.

Conclusion

Since 1957, Social Security disability benefits have been part of the American fabric, providing insured protection for those Americans who have paid into Social Security through their earnings. We must take the necessary steps in the near term to prevent the depletion of DI trust fund reserves and ensure that disability benefits continue to be paid in full to those Americans who have earned coverage and subsequently acquire a disability.

We thank you for your interest in this important program. We ask for your support for the President’s Budget request, which will reallocate payroll tax revenue to the DI trust fund and increase its reserves to a sufficient level until 2033, without risking the financial viability of either the OASI or DI Trust Funds, and without jeopardizing the benefits on which your constituents have come to depend. It would also invest in learning more about what strategies can help individuals with disabilities remain in the workforce, and would improve program integrity. Moving forward, we stand ready to assist the Congress regarding any Social Security proposals.

Again, thank you for the opportunity to testify today. I am glad to have our Chief Actuary, Stephen C. Goss, with me here today. We will be happy to answer any questions you may have.

___________________________________________

1 See http://www.ssa.gov/history/reports/trust/1995/.

2 For example, Congress reallocated payroll taxes from OASI to DI in the Tax Reform Act of 1969; from OASI to DI in the Social Security Amendments of 1973; from DI to OASI in the Allocation of Social Security Tax Receipts of 1980; from DI to OASI in the Social Security Amendments of 1983; and from OASI to DI in the Social Security Domestic Employment Reform Act of 1994.

3 To be insured for Social Security Disability, most individuals must have worked substantially in five out of the prior ten years before the onset of disability. This is in addition to the general 10-year (40 quarters) work requirement needed to gain “fully” insured status.

4 See http://www.ssa.gov/oact/STATS/table6c7.html.

5 For estimates of the number of Americans living with disabilities, including severe disabilities, see http://www.census.gov/prod/2012pubs/p70-131.pdf.

6 For more information about pre-effectuation reviews, see http://www.socialsecurity.gov/legislation/PER%20fy12.pdf.

7 In the SSI program, work incentives include more beneficial rules for counting income from earnings, the Plan to Achieve Self-Support, special rules about impairment-related work expenses, expedited reinstatement, and continued Medicaid.

8 A more comprehensive description of our work incentives is available at http://www.socialsecurity.gov/redbook/.